MANAGING SUPPLY CHAIN PERFORMANCE

|

|

|

- Claude Dupont

- il y a 8 ans

- Total affichages :

Transcription

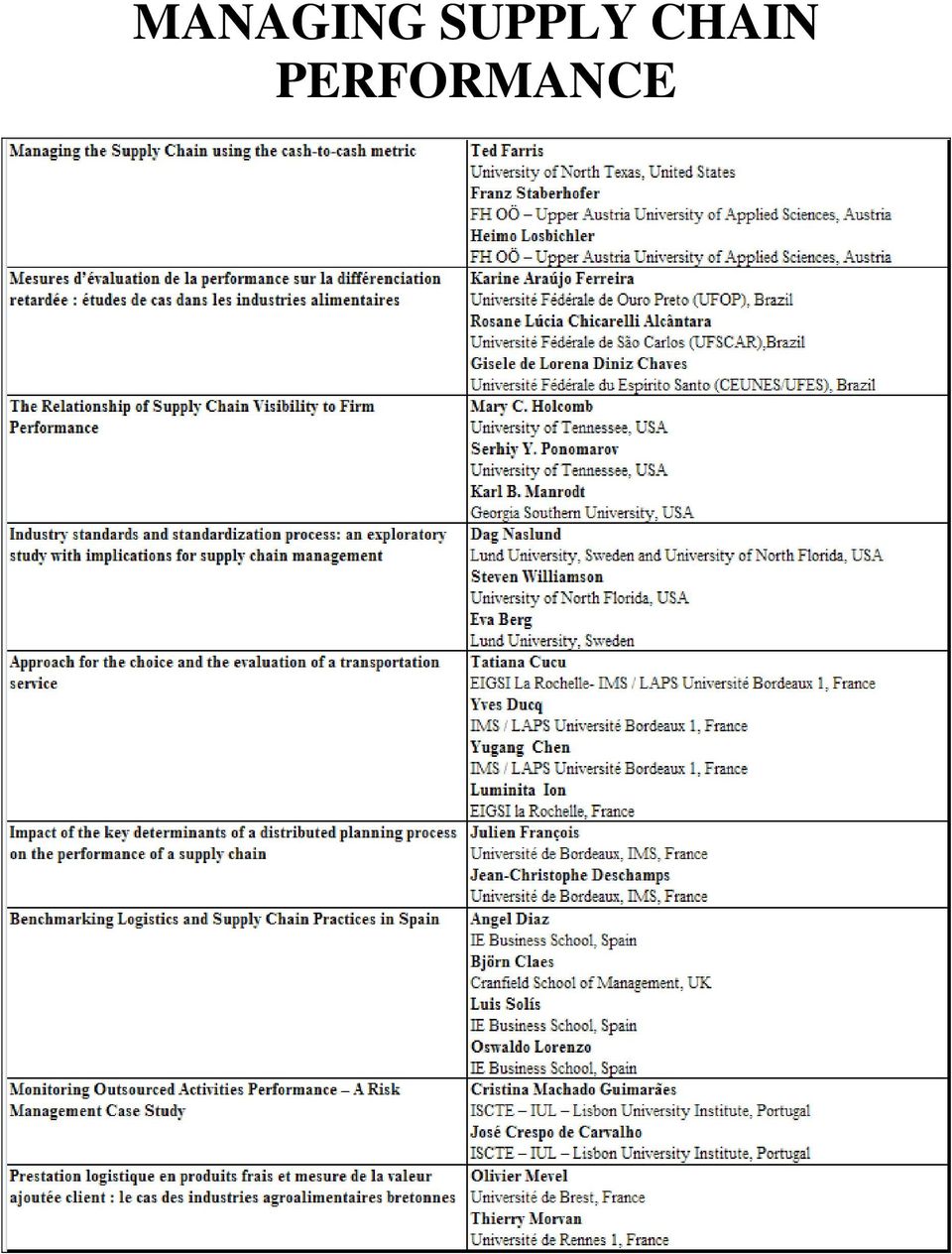

1 MANAGING SUPPLY CHAIN PERFORMANCE

2 RIRL Bordeaux September 30th & October 1st, 2010 RIRL 2010 The 8th International Conference on Logistics and SCM Research BEM Bordeaux Management School September 29, 30 and October 1st 2010 Managing the Supply Chain Using the Cash-to-Cash Metric Ted Farris University of North Texas, United States Farris@unt.edu Franz Staberhofer FH OÖ Upper Austria University of Applied Sciences, Austria Franz.Staberhofer@fh-steyr.at Heimo Losbichler FH OÖ Upper Austria University of Applied Sciences, Austria Heimo.Losbichler@fh-steyr.at Abstract There are many metrics available within a firm which may be used to help manage the firm toward achieving its objectives. Firms seeking supply chain improvements must develop metrics between firms. This paper provides an overview of the cash-to-cash concept. It begins by explaining how to calculate cash-to-cash. It then addresses the research question How can the cash-to-cash metric be used to help improve the profitability of the supply chain? First, it discusses how to leverage the three key variables to improve cash-to-cash performance. It considers the link between cash-to-cash performance and firm profitability as well as how to benchmark using the metric. Finally it identifies the premise behind WACC or inventory arbitrage and offers managerial considerations. Key words: cash conversion cycle, cash-to-cash, measurement, cash flow

3 RIRL Bordeaux September 30th & October 1st, : GENERAL OVERVIEW OF THE CASH-TO-CASH CONCEPT The concept of cash-to-cash is a basic financial concept. Cash-to-cash (C2C), or cash conversion cycle, is a composite metric that has been described as the average days required to turn a dollar invested in raw material into a dollar collected from a customer. (Stewart, 1995). Put another way, C2C is the length of time a company s cash is tied up in working capital before that money is finally returned when customers pay for the products sold or services rendered (Churchill & Mullins, 2001). C2C is a unique financial performance metric that indicates how a firm is managing their capital across the supply chain. 2: THE IMPORTANCE OF THE CASH-TO-CASH CONCEPT Companies are increasingly turning to inter-organizational alliances as a key business strategy to gain competitive advantages over traditional businesses attempting to go it alone. This trend, combined with the timeless challenge of effective cash flow management, motivates this assessment of cash-to-cash (C2C) strategies in a supply chain environment. This paper addresses the research question: How can the cash-to-cash metric be used to help improve the profitability of the supply chain? The cash-to-cash metric is important from both accounting and supply chain management perspectives: It can be used for accounting purposes in the determination of firm liquidity and organizational valuation. A shorter cash conversion cycle, implying that fewer days cash are tied up in working capital and not offset by "free" financing in the form of deferred payments, results in more liquidity for the firm (Soenen 1993). Also, a shorter conversion cycle results in a higher present value of net cash flows generated by the assets and therefore, a higher firm value. For supply chain management activities, the metric serves as a universal measurement bridging the processes into and out of the firm using common accounting measurements. As the management of the supply chain evolves managers will seek metrics that measure more than just dyadic relationships. The cash-to-cash metric involves three links in the supply chain. It bridges across inbound material or finished goods activities with suppliers, through manufacturing, wholesale and distribution operations, and continues through the outbound sales activities with customers bridges material activities with 2

4 RIRL Bordeaux September 30th & October 1st, 2010 suppliers, production operations, distribution functions, and outbound sales activities; it becomes one of the first multiadic metrics that may be used to further supply chain management. Todd Ackerman, director of the Performance Management Group states, "We find this metric of great value, and we emphasize it. Only one-third of the companies I encounter have any notion of it at all. The Chief Information Officer can use it to help create a dashboard, a series of metrics that drives the organizational behavior required to optimize the business model." (Slater 2000 Over the years, there have been several research studies that have examined C2C and its utilization by firms: Promoting Management Awareness - Beed (1981) suggests using the metric to spot inventory and accounts receivables problems. Byers et al, (1997) support using cash-tocash to manage operating assets. Hutchison and Farris (Today s CPA, 2004) and Hutchison et al, (CPA Journal, 2007) use it to guide accountants toward awareness. Performance and Benchmarking Indicator - Phillips (1999) cites cash-to-cash as an important key performance indicator. Farris & Hutchison (2002) proposed opportunities for extending cash-to-cash as a benchmark for supply chain management then (Hutchison & Farris 2003) compare cash-to-cash performance for benchmarking purposes for 5,884 companies across 31 industries. They also identified clear industry-wide changes within a petroleum supply chain (Hutchison & Farris, 2004) and Farris et al, (2005) used it to benchmark the retailing industry. Randall and Farris (2009) proposed opportunities for extending cash-to-cash as a benchmark for supply chain management. Link to Profitability and Creating Shareholder Value Soenen (1993), Ward (2004) and Skomorowsky (1988) linked cash-to-cash to profitability, earnings, and net income, respectively. Farris & Hutchison (2003) also identify the linkage. Losbichler, et al, (2008) blend cash-to-cash with EVA to identify how it may be used to create shareholder value. Optimizing Supply Chain Management - Hutchison et al, (2009) introduce what is now known as "WACC (weighted average cost of capital) or inventory arbitrage" to begin utilizing the cash-to-cash variables to help benefit the entire supply chain. Randall & 3

5 RIRL Bordeaux September 30th & October 1st, 2010 Farris (2009) further the arbitrage argument with examples using each of the key variables. This paper provides an overview of the cash-to-cash concept. It begins by explaining how to calculate cash-to-cash. It then begins to address the research question: How can the cash-tocash metric be used to help improve the profitability of the supply chain? by discussing how to leverage the three key variables to improve cash-to-cash performance. It considers the link between cash-to-cash performance and firm profitability as well as how to benchmark using the metric. Finally it identifies the premise behind WACC or inventory arbitrage and offers managerial considerations. 3: HOW TO CALCULATE CASH-TO-CASH Cash-to-cash is comprised of data readily available from publicly traded companies. The information can be gleaned from the firm s balance sheet and income statement such as the 2009 figures for Wal*Mart and Tesco shown in Table One. Table One Key Financial Figures Wal*Mart and Tesco FY2009 ($ Million) Wal*Mar Tesco t Annual Sales $408,214 $82,452 COGS $304,657 $76,051 Payables $30,451 $7,452 Inventory $33,160 $4,051 Receivables $4,144 $2,093 There are three key variables involved in the calculation of cash-to-cash: Accounts Payable, Inventory, and Accounts Payable. To calculate the measurement, first convert accounts payable, inventory, and accounts receivable into a common measurement represented in days. To convert accounts payable multiply dollars of accounts payable times the number of days in a year and then divide by the cost of goods sold. The result will be the number of days of accounts payable. Days of A/P = Accounts Payable x 365 = 30,451 x 365 = 36.5 days 4

6 RIRL Bordeaux September 30th & October 1st, 2010 COGS 304,657 Convert inventories using the same logic and the result will be the average number of days of inventory in your system. Days of Inventory = Inventory x 33,160 x = COGS 304,657 = 39.7 days To convert accounts receivable multiply dollars of accounts receivable times the number of days in a year and then divide by sales. Keep in mind that your receivables are based on the sales price but the payables and inventories are based on the cost of goods sold sans profit. Days of A/R = Accounts Receivable x 4,144 x = Sales 408,214 = 3.7 days Use these converted variables to calculate cash-to-cash by adding days of accounts receivables to days of inventories and subtracting days of accounts payable. Days of A/R + Days of Inventory Days of A/P = Days of Cash-to-Cash 3.7 Days Days 36.5 days = 7.0 Days of Cash-to-Cash The result standardizes the data into days and may be either a positive or a negative number. A positive result indicates the number of days your cash is used to finance inventory. A negative result indicates the number of days you have received cash from sales before supplier payment for inventory is required. Ultimately, the goal for most firms is a C2C as close to zero (or negative) as reasonable for a company in that particular industry. A lower C2C suggests that a firm is more efficient, since it turns its working capital over more times per year and generates more sales per money invested. It should be noted that the C2C calculation assumes that cycle time may be shortened without a resulting increase in costs or decrease in sales (Soenen 1993). Cash-to-cash may be depicted graphically as shown in Figure One. Both firms shown have almost the same number of days payables (Tesco 35.8 days; Wal*Mart 36.5 days). Even though it takes longer to receive payment from its customers, Tesco is able to offset this difference by conducting its business with half of the inventories of Wal*Mart. The net C2C situation is 14.1 days better for Tesco and a higher profit margin. Since each variable must be 5

7 RIRL Bordeaux September 30th & October 1st, 2010 viewed in the context of a firm s mission and market, interpretation of these results is limited; yet examining all three variables in combination provides a clear understanding of C2C for a company. 6

8 RIRL Bordeaux September 30th & October 1st, 2010 Figure One Graphic Representation of Cash-to-Cash 4: MANAGING WITH CASH-TO-CASH Many firms are aware of the merits of computing their C2C. The underlying attraction of improving C2C is that a reduction in C2C days will lead to operational and financial improvement. Each firm seeks to obtain a proper mix between the amount of resources deployed to working capital and those to capital investments. Thus, there is an on-going trade-off between operational decisions to lengthen the C2C cycle (which increases liquidity required), and financial decisions to shorten the cycle (which decreases liquidity required). There are many managerial implications to using the C2C metric. First, it serves as a measure of change across time for variables that reach across functional silos. Dell Computer Company reports C2C changes in the company quarterly financial reports to the stockholders. Second, it can be beneficial as a means of setting goals for improvement within the firm and the supply chain. Third, it may be beneficial as a means of setting cross-functional goals for the company. Fourth, it is critical for the manager to understand the company s performance relative to companies within the same industry. Fifth, understanding how the metric has changed over the years, offers insights about which variables offer the greatest leverage 7

, and financial decisions to shorten the cycle (which decreases")

9 RIRL Bordeaux September 30th & October 1st, 2010 points and opportunities for improvement. Even if an individual company does not manage its C2C, their suppliers and customers may use it and their actions will directly impact the firm that does not. Managing the C2C cycle involves an effort that should have both a crossfunctional approach within the company and a collaborative approach between the company, immediate customers, and immediate suppliers. Many of the successful management techniques to improve C2C are a result of implementing basic principles. The biggest concern of cash-to-cash management is the potential for one firm to suboptimize the supply chain by improving their cash-to-cash numbers at the expense of trading partners. Doing so may threaten the financial livelihood of the partners, by increasing their costs or potentially driving them into bankruptcy. It is important, therefore, to collaboratively utilize this metric through such activities as WACC or inventory arbitrage for the good of the supply chain to drive down costs, share risk, and increase profitability. There are three primary leverage points to manage cash-to-cash: extending Accounts Payable days, reducing Inventory days, and reducing Accounts Receivable collection days. Adjustments to these variables must be considered collectively, since changes in one variable do not have a one-to-one day relationship with the others. In today s highly competitive global supply chains, enlightened managers recognize that actions which do not consider the ethical and financial consequences of their decisions may lead to adverse consequences ranging from adverse publicity to having suppliers and customers abandon them. 4.1: Extend Average Accounts Payable One approach to improving the cash-to-cash metric is to extend average accounts payable associated with inventory and therefore, obtain interest-free financing. There are many ways to accomplish this. A firm can utilize electronic payment for raw materials, inventory, wages, and expenses so that payment is made at the last possible date. A firm may also make scheduled partial payments rather than one full payment. Consider changing the frequency of employee payroll payments from weekly to monthly. An additional idea would be to extend payments by utilizing interest-free credit cards or lines of credit. Finally, sales commissions could be credited when accounts receivables are paid rather than at point of sale (Walz 1999). The goal 8

10 RIRL Bordeaux September 30th & October 1st, 2010 of all the strategies is to control and limit disbursement of cash until the last possible moment. See Boardman & Ricci (1985), Schaeffer (2007), and Bates et al, (2009) for further opportunities. 4.2: Reduce Inventory Days of Inventory Many outside the firm view inventory as a barometer of efficiency. Specifically, evaluations should be made regularly regarding Reorder Points (ROP) and Economic Order Quantities (EOQ). Many inventory strategies can be utilized to improve this variable for the C2C model. These include: real-time inventory tracking, Collaborative Planning, Forecasting, and Replenishment (CPFR), and synchronizing supply/demand planning. For example, using advanced technology such as RFID and its associated hardware and software to provide realtime inventory information throughout the supply chain can be a win-win for all members. Not only can total inventory in the system be reduced, but sales can grow as the in-stock rate increases. Consider the overall supply chain impact of shifting inventory in the supply chain. 4.3: Reduce Average Accounts Receivable Expediting receivables collections is the final leverage point for improving the cash-to-cash metric. While the objective with accounts payable was to control and limit the expenditure of cash until the last possible moment, the goal with accounts receivable is to speed cash collection. The days-sales-outstanding term captures the ratio of accounts receivable to average-daily sales and thus provides a "days" measure of outstanding receivables (Stewart 1995). To encourage faster payments, discount terms appear to be the one of the most effective mechanisms to increase receivables collection (Boardman and Ricci, 1985). There is also evidence that companies with low days-sales-outstanding tend to follow up quickly on delinquent accounts (Stewart 1995). Further, interest could be assessed on delinquent accounts and future orders for delinquent customers could require COD (Cash On Delivery) payments. Other approaches for expediting receivables include using lock boxes, where post office boxes are obtained in close proximity to customers, the boxes are serviced daily, and deposits made with banks to company accounts. Another idea is to require full payment at time of 9

and Economic Order Quantities (EOQ).")

11 RIRL Bordeaux September 30th & October 1st, 2010 order or to require a large deposit. Acceptance of electronic payments from customers allowing for automatic deposit of payments would also expedite receivables. Or in today s environment, require electronic transfer so there is no float. Additionally, customers could be provided pre-addressed, stamped envelopes (Walz 1999). While these suggestions for improving the C2C variables are not all-inclusive, implemented separately or together they can improve cash-to-cash. Firms are encouraged to determine their own approaches to improving C2C and its variables within the context of their firm s mission and market. 5: CASH-TO-CASH AND PROFITABILITY Soenen (1993), Ward (2004) and Skomorowsky (1988) linked cash-to-cash to profitability, earnings, and net income, respectively. Farris & Hutchison (2003) also identify the linkage. Losbichler et al, (2008) blend cash-to-cash with EVA to identify how it may be used to create shareholder value. Preliminary work by the author investigating the relationship between cash-to-cash performance and profitability has determined that 20 out of 30 industries investigated had a direct relationship where better cash-to-cash performance directly correlated to higher profitability. Seeking to determine causes, the author initially considered those industries where there is not a direct correlation. The industry with the best cash-to-cash performance, Eating and Drinking Places, did not have a direct correlation of profitability to performance. It can be conjectured that the reason behind this lack of relationship is that due to the nature of the industry all participants operate utilizing the same logistics model; food needs to be fresh (thus lower inventories), receivables tend to be handled the same regardless of the level or prestige of the restaurant, and the traditional invoice-check accounts payable system is universal. Further investigation in this area is merited to draw more concrete conclusions. 6.0 BENCHMARKING USING CASH-TO-CASH The C2C measures may also offer useful and readily available benchmarking data. Farris & Hutchison (2002) proposed opportunities for extending cash-to-cash as a benchmark for 10

12 RIRL Bordeaux September 30th & October 1st, 2010 supply chain management then (Hutchison & Farris 2003) compare cash-to-cash performance for benchmarking purposes for 5,884 companies across 31 industries. They also identified clear industry-wide changes within a petroleum supply chain (Hutchison & Farris, 2004). Farris et al, (2005) used it to benchmarking the retailing industry. Randall & Farris (2009) proposed opportunities for extending cash-to-cash as a benchmark for supply chain management. Firms in the past had difficulty obtaining financial data from other companies and coming up with benchmarks. The earliest known compilation of benchmark C2C measurements features data from a study by Pitiglio, Rabin, Todd, & McGrath (2000) which summarized the metric for more than 320 technology-based companies. Today, data is readily available and computer technology expedites the computation of any public firm s C2C. Data may also be obtained from trade organizations such as WERC (Food Logistics, 2008). Professionals seeking to improve the supply chain with their suppliers and customers may use C2C as a benchmark to begin investigation of opportunities. The process for improvement as described in Hutchison et al, (2007) includes: Step 1: Step 2: Step 3: Step 4: Step 5: Step 6: Determine C2C variables for the company as well as competitors in the same industry. Benchmark company position relative to their respective industry. Compare company performance and determine where there are large differences from industry leaders. Quantify the value of changing one day for each variable. Determine C2C variables for key suppliers and key customers. Identify where there are significant differences between trading partners for offsetting variables (Accounts Receivable vs. Accounts Payable). Determine the financial impact of aligning (changing) the offsetting variables and seek a gain/gain share with trading partners. 6.1: Benchmarking By Industry Each industry will differ in their cash-to-cash performance. It is possible to group some industries based upon each specific variable. (See Farris & Hutchison 2003 for groupings). 11

13 RIRL Bordeaux September 30th & October 1st, 2010 For example, the Construction Industry has a high number of days of inventory (time to construct a building can accumulate inventories for up to 6 months), low accounts payable (since work crews tend to be paid on a weekly or sometimes daily basis) and low accounts receivable (builder is paid quickly by the finance company after the sale is completed). The industry with the best cash-to-cash performance is Eating and Drinking Places with the shortest average cash-to-cash performance of any industry at -8.2 days. The reason is the nature of the business; most restaurants have fresh food so the average days of supply of inventory are low. Customers tend to pay for meals with cash or credit cards so accounts receivables are low, and suppliers are paid through the traditional invoice-check method. 6.2: Benchmarking By Company One may drill down even further to investigate how a company is performing within a specific industry. Consider where your company is positioned overall in the industry and seek out primary difference between the better performers and your company as an indicator of potential changes in your business practice. 7: GUIDING SUPPLY CHAIN MANAGEMENT MANAGERIAL IMPLICATIONS As management of the supply chain continues to evolve, the cash-to-cash metric is one of the currently available measurement tools to transform the relationships between firms and functions of the supply chain into a value chain by helping to synergistically optimize the entire process through a systems approach. One of the most important aspects of supply chain management involves increasing the efficiency of financial (funds) flows throughout the chain. The quicker goods move through the supply chain, the faster members will be paid, which increases cash flow. To examine this process in more detail, the C2C process needs to be further understood. Hutchison et al, (2009) introduce what is now known as "WACC or inventory arbitrage" to begin utilizing the cash-to-cash variables to help benefit the entire supply chain. Randall & Farris (2009) further the arbitrage argument with examples using each of the key variables. Because chain members have differing cost and revenue structures, they also have heterogeneous gains in capturing benefits from collaboration (Lee 2000). Using the precept that one company s accounts payable is another company s account receivable, and that each 12

14 RIRL Bordeaux September 30th & October 1st, 2010 company holds inherent advantages (such as lower weighted average cost or lower inventory carrying cost), there are opportunities to further manage the supply chain. Through proper management of these relationships, these inherent advantages can be used to the benefit of both trading partners. By working in an integrated fashion to shift costs to the company with the inherent advantage, profits are increased for all companies, and total supply chain costs can be reduced. In addition, new delivery channels for remittances (Isaacs 2009), online, prepaid cards, and mobile, offer additional use of technology to manage faster payment. If used properly, the cash-to-cash metric may result in reduced supply chain structure costs, increasing profitability for supply chain partners, and potentially driving out cost for the end consumer. 8: SUGGESTIONS FOR FUTURE RESEARCH There are many research questions that may be addressed to assist firm management and enhance C2C. An important research question would be to determine how outside influences such as technology and the economy have influenced improvements of the key variables of C2C. Future analysis within industries themselves may also offer further knowledge into developing realistic expectations of the C2C metric based on a particular industry, type of supply chain or business process, product value, and size of a company. As C2C permeates through the supply chain, there are also research questions to explore concerning power in the channel and the influence of cash management on a trading partner s C2C cycle and profitability. For companies that appear to be very successful in terms of their C2C cycles, case based research could provide insights beyond that gained from analysis financial data. 9: CONCLUSIONS The cash-to-cash metric is becoming an important measure as it bridges across inbound material activities with suppliers, through operations, and the sales and outbound logistics activities with customers. This paper provided an overview of the cash-to-cash concept. It began by explaining how to calculate cash-to-cash then addressed the research question: How can the cash-to-cash metric be used to help improve the profitability of the supply chain? It discussed how to leverage the three key variables to improve cash-to-cash performance. It considered the link between cash-to-cash performance and firm profitability 13

, online, prepaid cards, and mobile, offer additional use of technology to manage faster payment.")

15 RIRL Bordeaux September 30th & October 1st, 2010 as well as how to benchmark using the metric. Finally it identified the premise behind WACC or inventory arbitrage and offered managerial considerations. Research suggests that each firm may possess comparative advantage in its weighted average cost of capital (WACC) or inventory carrying cost (ICC), that may be exploited synergistically throughout the supply chain (Moss & Stine, 1993).Cash-to-cash may be used as the primary driver to identify opportunities. By sharing data, all trading partners may realize efficiencies that ultimately improve their cash flows and profitability. 10: ENDNOTES Warehouse Metrics Study Available From WERC, Food Logistics, June 2008, Issue 105, p.8. Bates, Thomas W., Kahle, Kathleen M., and Rene M. Stulz, (2009) Why Do U.S. Firms Hold So Much More Cash than They Used To? Journal of Finance, October, Volume 64 Issue 5, pp Beed, Teresa, (1981) Using Operating Cycle Figures To Spot Inventory And Accounts Receivable Problems, Montana Business Quarterly, Volume 19, No 3 (Autumn), p. 23. Boardman, Calvin M. and Kathy J. Ricci, (1985) Defining Selling Terms: Economics Of Delaying Payment-How Does Your Industry Compare?, Credit & Financial Management, Volume 87, No. 3, pp Byers, Steve S., John C. Groth, and Marilyn K. Wiley, (1997) Managing Operating Assets To Create Value, Management Decision, Volume 35, No. 2, p.133. Churchill, Neil C., and John W. Mullins, (2001) How Fast Can Your Company Afford To Grow? Harvard Business Review, May, pp Farris II, M. Theodore and Paul D. Hutchison, (2002) Cash-To-Cash: The New Supply Chain Management Metric, International Journal of Physical Distribution & Logistics Management, Volume 32, No s 3-4, pp Farris II, M. Theodore and Paul D. Hutchison, (2003) Measuring Cash-To-Cash Performance, The International Journal of Logistics Management, Volume 14, No. 2, pp Farris, M. Theodore, Paul D. Hutchison, and Ronald W. Hasty, (2005) Using Cash-to-Cash To Benchmark Service Industry Performance Journal of Applied Business Research. Volume 21, No. 2, pp H. L. Lee, (2000) Creating value through supply chain integration, Supply Chain Management Review, September/October, pp.30-36; as cited in T. M. Simatupang and R. Sridharan. (2005) An integrative framework for supply chain collaboration, The International Journal of Logistics Management, Volume 16, No. 2, pp Hutchison, Paul and M. Theodore Farris II, (2003) Cash-to-Cash In The Oil Industry: Assessment and Benchmarks, Oil, Gas, and Energy Quarterly, Volume 51, No. 3, pp

.Cash-to-cash may be used as the primary driver to identify opportunities.")

16 RIRL Bordeaux September 30th & October 1st, Hutchison, Paul D. and M. Theodore Farris II, (2004) Managing The Cash-To-Cash Cycle To Increase Firm Value, Today s CPA, Volume 31, No. 5 (March/April), pp Hutchison, Paul D., M. Theodore Farris, and Susan B. Anders, (2007) Cash-to-Cash Analysis and Management, CPA Journal. August, pp Hutchison, Paul D., Farris II, M. Theodore, and Gary M. Fleischman (2009) Supply Chain Cash-to-Cash, Strategic Finance, July, Volume 91 Issue 1, pp Isaacs, Leon (2009) New delivery channels for remittances: Where do the opportunities lie? How will new technologies change the face of this rapidly expanding market? Journal of Payments Strategy & Systems, August, Volume 3 Issue 3, pp Losbichler, Heimo, Mahmoodi, Farzadand Markus Rothboeck (2008) Creating Greater Shareholder Value from Supply Chain Initiatives, Supply Chain Forum: International Journal, Volume 9 Issue 1, pp Moss, J.D. and Stine, B. (1993), "Cash conversion cycle and firm size: a study of retail firms", Managerial Finance, Volume 19 No. 8, pp Pitiglio, Rabin, Todd, & McGrath (PRTM), (2000) PRTM Survey: Top Performers Cut SCM Costs To 4% Of Sales, MDM 29.16, Aug The Performance Measurement Group, LLC (PMG), a subsidiary of management consultants PRTM, released results of the first survey in its online Supply-Chain Management Benchmarking Series ( Randall, Wesley S. and M. Theodore Farris, (2009) Supply Chain Financing: Using Cash-to- Cash Variables to Help Align the Supply Chain The International Journal of Physical Distribution & Logistics Management. Volume 39, No. 8, pp Randall, Wesley S., and M. Theodore Farris, (2009) Utilizing Cash-to-Cash to Benchmark Company Performance Journal of Benchmarking, Volume 16, Issue 4, pp Schaeffer, Mary S, (2007) Using accounts payable to improve cash flow, Journal of Corporate Accounting & Finance, November/December, Volume 19 Issue 1, pp Skomorowsky, Peter, (1988) The Cash To Cash Cycle And Net Income, The CPA Journal, Volume 58, No. 12 (December), pp Slater, Derek, (2000) By The No s, Supply Chain Best Practices Issue of CIO Magazine, Volume 13, No. 16 (June 1), p.34. Soenen, Luc A., (1993) Cash Conversion Cycle And Corporate Profitability, Journal Of Cash Management, Volume 13, No.. 4, p.53. Stewart, Gordon, (1995) Logistics Supply Chain Performance Benchmarking Study Reveals Keys To Supply Chain Excellence, Information Management Volume 8, No.. 2, pp Walz, D., (1999) On-Line Lecture, ( Ward, Peter, (2004) Cash-To-Cash Is What Counts, Journal of Commerce, (February 16), p.1. 15

New delivery channels for remittances: Where do the opportunities lie? How will new technologies change the face of this rapidly expanding market?")

17 RIRL Bordeaux September 30th & October 1st, 2010 RIRL 2010 The 8th International Conference on Logistics and SCM Research BEM Bordeaux Management School September 29, 30 and October 1st 2010 Mesures d évaluation de la performance sur la différenciation retardée: études de cas dans les industries alimentaires Karine Araújo Ferreira Université Fédérale de Ouro Preto (UFOP) - Brésil karine@decea.ufop.br Rosane Lúcia Chicarelli Alcântara Université Fédérale de São Carlos (UFSCAR) - Brésil rosane@dep.ufscar.br Gisele de Lorena Diniz Chaves Université Fédérale du Espírito Santo (CEUNES/UFES) - Brésil giselechaves@ceunes.ufes.br Résumé La différenciation retardée, qui consiste à repousser la configuration finale et/ou le déplacement de produits jusqu à ce que la commande du consommateur soit reçue, est une stratégie qui a connue une montée en puissance ces dernières années. Ce travail cherche comment la différenciation retardée est appliquée dans les entreprises de l industrie alimentaire et quelles sont les mesures de performance passibles d être utilisées afin d évaluer les résultats de son application. A cette fin, six études de cas ont été menées dans des entreprises productrices de jus et de fruits en conserves. Parmi les résultats obtenus, il est décrit les mesures de performance identifiées dans l évaluation de la différenciation retardée. Mots-clés: mesures de performance, différenciation retardée, industrie alimentaire. 1

- Brésil giselechaves@ceunes.ufes.")

18 RIRL Bordeaux September 30th & October 1st, Introduction Le milieu socio-économique actuel mondial exige des chaînes d approvisionnement d être capables de s adapter et de répondre rapidement aux marchés caractérisés par des exigences telles que : minimisation des coûts, différenciation des produits, fiabilité, réduction des délais de livraison, amélioration du contrôle de la qualité, grande flexibilité et diversité. Dans ce sens, la gestion de la chaîne d approvisionnement ou Supply Chain Management (SCM) se distingue en introduisant des nombreuses initiatives et pratiques qui ont changé les façons de faire et de gérer les processus des affaires tout au long de la chaîne d approvisionnement. Parmi ces initiatives et pratiques vérifiées, se trouve la différenciation retardée, qui consiste à retarder au maximum la configuration finale et / ou déplacement de produits et services, jusqu à ce que la demande soit connue. L objectif est d avoir un produit commun (ou base) dans la chaîne d approvisionnement pour la phase de production poussée et de procéder à la différenciation au plus près possible de la production tirée. Ces dernières années, le sujet a attiré l attention de nombreux chercheurs et professionnels de pays différents. Depuis que le concept de différenciation retardée à été défini dans la littérature de marketing par Alderson en 1950, plusieurs travaux traitant du sujet peuvent être rencontrés dans divers secteurs comme la logistique, la production, le projet de produit et plus récemment, dans la chaîne d approvisionnement (YANG et al., 2004a). Malgré l attention croissante apportée au sujet, son application pratique est encore réduite et la plupart des études se limitent à des révisions théoriques ou à l élaboration de modèles mathématiques et de simulation. De plus, les résultats de son application sont peu connus, et plus particulièrement dans l industrie alimentaire brésilienne où le concept est encore peu discuté. Une des principales causes de cette méconnaissance des impacts stratégiques est due, entre autre, au manque de mesure de performance pour évaluer la différenciation retardée dans les entreprises. Malgré les recherches de nombreux auteurs décrivant les différentes mesures d évaluation de la performance logistique et de la chaîne d approvisionnement, il existe peu de travaux qui préconisent l utilisation de mesures adéquates pour évaluer l impact sur des stratégies comme la différenciation retardée. Ainsi cette étude cherche à répondre comment la stratégie de différenciation retardée est appliquée dans les entreprises de l industrie alimentaire et quelles mesures de performance peuvent être utilisées pour évaluer les résultats de son application. Pour atteindre les objectifs de cette recherche, six études de cas exploratoires ont été menées dans des entreprises de fabrication de jus et de fruits en conserves, sachant que trois d entre elles ont comme principale activité la fabrication de jus d orange et trois autres, la fabrication de dérivés de 2

se distingue en introduisant des nombreuses initiatives et pratiques qui ont changé les façons de faire et")

19 RIRL Bordeaux September 30th & October 1st, 201 tomate. Des entrevues personnelles ont été réalisées dans chaque entreprise, la plupart avec les responsables des activités des secteurs de la production et de la logistique. La deuxième partie de cet article présente les principaux concepts et variantes de différenciation retardée identifiés par la révision de la littérature. Ensuite, dans une troisième partie, il est décrit l évaluation de la performance de la différenciation retardée, détaillant les principales mesures de performance pour évaluer cette stratégie, identifiées dans la littérature. Les résultats de ces études de cas réalisées dans les six entreprises de jus et de fruits en conserve sont analysés dans une quatrième partie. Enfin seront présentées les considérations finales du travail, et suivront les références bibliographiques. 2 Différentiation retardée : définition et variantes La différenciation retardée est une pratique de plus en plus répandue dans la littérature académique et dans ses applications pratiques. Le concept fut initialement proposé par Alderson (1950) comme une solution pour changer la forme, l identité ou la localisation de produits le plus tard possible dans les processus de fabrication et de distribution physique. L objectif était de réduire les risques liés à la manutention des produits en les centralisant jusqu au dernier instant possible ou en les maintenant indifférenciés jusqu au dernier point du flux des marchandises. Ainsi, retarder le déplacement du produit fut appelé «différenciation retardée dans le temps» (time postponement), alors que dans le cas du produit elle fut nommée «différenciation retardée de la forme» (form postponement). En 1965, Bucklin incorpora plus de détails au travail d Alderson, il a étudié les limites de l application de la stratégie et créa le concept opposé à la différenciation retardée, le Principe de la Spéculation (Principle of Speculation). Le principe consiste à finaliser les opérations le plus tôt possible dans le procédé de fabrication (BUCKLIN, 1965). Les travaux d Alderson et Bucklin sur la différenciation retardée étaient visionnaires à l époque, mais les lead times de la production et de la distribution ont rendu difficile l application du concept et n ont pas reçu toute l attention méritée des industriels de l époque. Après 1965, peu de travaux ont traité le sujet, et le thème a été traité seulement à partir des années 80 par Zinn et Bowersox (1988) qui proposèrent que la différenciation retardée soit séparée en cinq éléments distincts, chacun avec sa propre structure. En plus de la différenciation retardée dans le temps, l auteur formalise quatre types de différenciations retardées de la forme, à savoir : 3

20 RIRL Bordeaux September 30th & October 1st, 201 Différenciation retardée d étiquetage : dans cette stratégie, les produits sont stockés sans étiquette identifiant la marque. Celle-ci est seulement fixée une fois que le produit est vendu sous une des différentes marques que l entreprise possède. Différenciation retardée d emballage : le produit n est emballé qu après avoir été vendu, selon sa taille, la quantité ou le type d emballage. Différenciation retardée du montage : dans ce cas, ce n est pas seulement l emballage, le montage du produit est lui aussi retardé jusqu à ce que l entreprise reçoive la commande du client. Différenciation retardée de la fabrication : seule la fabrication est réalisée après la réception de la commande. Bowersox et Closs (1996) définissent deux types de différenciation retardée : la différenciation retardée de fabrication (ou de la forme) et la différenciation retardée logistique (dans le temps). La première consiste à fabriquer un produit de base ou standard en quantité suffisante pour réaliser des économies d échelle, et à réaliser les caractéristiques finales à partir des commandes passées par les consommateurs. Le deuxième type consiste lui à centraliser les stocks des différents types de produits finis, et lorsque la commande est passée, les produits sont transportés directement au distributeur ou au consommateur. Pagh et Cooper (1998) s accordèrent sur quatre stratégies de différenciation retardée, pour la chaîne de distribution, dans une matrice 2x2 (Figure 1). Cette matrice, différenciation retardée de la forme, est appelée différenciation retardée de fabrication (manufacturing postponement) et différenciation retardée dans le temps est appelée différenciation retardée logistique (logistics postponement). Ces quatre stratégies sont donc une combinaison entre la différenciation retardée de fabrication et de la logistique appelée également de différenciation retardée totale, dans le cas contraire elle sera nommée de stratégie de spéculation complète. Il est important de préciser que le choix de la meilleure stratégie est contraint par la position du Point de Pénétration de Commande. LOGISTIQUE Spéculation Stocks décentralisés Différenciation retardée Stocks centralisés et distribution directe FABRICATION Spéculation Fabrication sur stock Différenciation retardée Fabrication sur commandes Stratégie de spéculation totale Stratégie de différenciation retardée de fabrication Stratégie de différenciation retardée logistique Stratégie de différenciation retardée totale 4

EN UNE PAGE PLAN STRATÉGIQUE

EN UNE PAGE PLAN STRATÉGIQUE PLAN STRATÉGIQUE EN UNE PAGE Nom de l entreprise Votre nom Date VALEUR PRINCIPALES/CROYANCES (Devrait/Devrait pas) RAISON (Pourquoi) OBJECTIFS (- AN) (Où) BUT ( AN) (Quoi)

EN UNE PAGE PLAN STRATÉGIQUE PLAN STRATÉGIQUE EN UNE PAGE Nom de l entreprise Votre nom Date VALEUR PRINCIPALES/CROYANCES (Devrait/Devrait pas) RAISON (Pourquoi) OBJECTIFS (- AN) (Où) BUT ( AN) (Quoi)

Nouveautés printemps 2013

» English Se désinscrire de la liste Nouveautés printemps 2013 19 mars 2013 Dans ce Flash Info, vous trouverez une description des nouveautés et mises à jour des produits La Capitale pour le printemps

» English Se désinscrire de la liste Nouveautés printemps 2013 19 mars 2013 Dans ce Flash Info, vous trouverez une description des nouveautés et mises à jour des produits La Capitale pour le printemps

Tier 1 / Tier 2 relations: Are the roles changing?

Tier 1 / Tier 2 relations: Are the roles changing? Alexandre Loire A.L.F.A Project Manager July, 5th 2007 1. Changes to roles in customer/supplier relations a - Distribution Channels Activities End customer

Tier 1 / Tier 2 relations: Are the roles changing? Alexandre Loire A.L.F.A Project Manager July, 5th 2007 1. Changes to roles in customer/supplier relations a - Distribution Channels Activities End customer

Instructions Mozilla Thunderbird Page 1

Instructions Mozilla Thunderbird Page 1 Instructions Mozilla Thunderbird Ce manuel est écrit pour les utilisateurs qui font déjà configurer un compte de courrier électronique dans Mozilla Thunderbird et

Instructions Mozilla Thunderbird Page 1 Instructions Mozilla Thunderbird Ce manuel est écrit pour les utilisateurs qui font déjà configurer un compte de courrier électronique dans Mozilla Thunderbird et

APPENDIX 6 BONUS RING FORMAT

#4 EN FRANÇAIS CI-DESSOUS Preamble and Justification This motion is being presented to the membership as an alternative format for clubs to use to encourage increased entries, both in areas where the exhibitor

#4 EN FRANÇAIS CI-DESSOUS Preamble and Justification This motion is being presented to the membership as an alternative format for clubs to use to encourage increased entries, both in areas where the exhibitor

We Generate. You Lead.

www.contact-2-lead.com We Generate. You Lead. PROMOTE CONTACT 2 LEAD 1, Place de la Libération, 73000 Chambéry, France. 17/F i3 Building Asiatown, IT Park, Apas, Cebu City 6000, Philippines. HOW WE CAN

www.contact-2-lead.com We Generate. You Lead. PROMOTE CONTACT 2 LEAD 1, Place de la Libération, 73000 Chambéry, France. 17/F i3 Building Asiatown, IT Park, Apas, Cebu City 6000, Philippines. HOW WE CAN

RÉSUMÉ DE THÈSE. L implantation des systèmes d'information (SI) organisationnels demeure une tâche difficile

organisationnels demeure une tâche difficile") RÉSUMÉ DE THÈSE L implantation des systèmes d'information (SI) organisationnels demeure une tâche difficile avec des estimations de deux projets sur trois peinent à donner un résultat satisfaisant (Nelson,

RÉSUMÉ DE THÈSE L implantation des systèmes d'information (SI) organisationnels demeure une tâche difficile avec des estimations de deux projets sur trois peinent à donner un résultat satisfaisant (Nelson,

MANAGEMENT SOFTWARE FOR STEEL CONSTRUCTION

Ficep Group Company MANAGEMENT SOFTWARE FOR STEEL CONSTRUCTION KEEP ADVANCING " Reach your expectations " ABOUT US For 25 years, Steel Projects has developed software for the steel fabrication industry.

Ficep Group Company MANAGEMENT SOFTWARE FOR STEEL CONSTRUCTION KEEP ADVANCING " Reach your expectations " ABOUT US For 25 years, Steel Projects has developed software for the steel fabrication industry.

Natixis Asset Management Response to the European Commission Green Paper on shadow banking

European Commission DG MARKT Unit 02 Rue de Spa, 2 1049 Brussels Belgium markt-consultation-shadow-banking@ec.europa.eu 14 th June 2012 Natixis Asset Management Response to the European Commission Green

European Commission DG MARKT Unit 02 Rue de Spa, 2 1049 Brussels Belgium markt-consultation-shadow-banking@ec.europa.eu 14 th June 2012 Natixis Asset Management Response to the European Commission Green

INDIVIDUALS AND LEGAL ENTITIES: If the dividends have not been paid yet, you may be eligible for the simplified procedure.

Recipient s name 5001-EN For use by the foreign tax authority CALCULATION OF WITHHOLDING TAX ON DIVIDENDS Attachment to Form 5000 12816*01 INDIVIDUALS AND LEGAL ENTITIES: If the dividends have not been

Recipient s name 5001-EN For use by the foreign tax authority CALCULATION OF WITHHOLDING TAX ON DIVIDENDS Attachment to Form 5000 12816*01 INDIVIDUALS AND LEGAL ENTITIES: If the dividends have not been

Le marketing appliqué: Instruments et trends

Le marketing appliqué: Instruments et trends Björn Ivens Professeur de marketing, Faculté des HEC Université de Lausanne Internef 522 021-692-3461 / Bjoern.Ivens@unil.ch Le marketing mix Produit Prix Communication

Le marketing appliqué: Instruments et trends Björn Ivens Professeur de marketing, Faculté des HEC Université de Lausanne Internef 522 021-692-3461 / Bjoern.Ivens@unil.ch Le marketing mix Produit Prix Communication

Comprendre l impact de l utilisation des réseaux sociaux en entreprise SYNTHESE DES RESULTATS : EUROPE ET FRANCE

Comprendre l impact de l utilisation des réseaux sociaux en entreprise SYNTHESE DES RESULTATS : EUROPE ET FRANCE 1 Objectifs de l étude Comprendre l impact des réseaux sociaux externes ( Facebook, LinkedIn,

Comprendre l impact de l utilisation des réseaux sociaux en entreprise SYNTHESE DES RESULTATS : EUROPE ET FRANCE 1 Objectifs de l étude Comprendre l impact des réseaux sociaux externes ( Facebook, LinkedIn,

Application Form/ Formulaire de demande

Application Form/ Formulaire de demande Ecosystem Approaches to Health: Summer Workshop and Field school Approches écosystémiques de la santé: Atelier intensif et stage d été Please submit your application

Application Form/ Formulaire de demande Ecosystem Approaches to Health: Summer Workshop and Field school Approches écosystémiques de la santé: Atelier intensif et stage d été Please submit your application

Règlement sur le télémarketing et les centres d'appel. Call Centres Telemarketing Sales Regulation

THE CONSUMER PROTECTION ACT (C.C.S.M. c. C200) Call Centres Telemarketing Sales Regulation LOI SUR LA PROTECTION DU CONSOMMATEUR (c. C200 de la C.P.L.M.) Règlement sur le télémarketing et les centres d'appel

THE CONSUMER PROTECTION ACT (C.C.S.M. c. C200) Call Centres Telemarketing Sales Regulation LOI SUR LA PROTECTION DU CONSOMMATEUR (c. C200 de la C.P.L.M.) Règlement sur le télémarketing et les centres d'appel

Cegedim. Half-year results

Cegedim Half-year results September 24, 2010 Contents A strategy focused on healthcare Delivering strong results A strong financial structure Additional information 2 A strategy focused on healthcare 3

Cegedim Half-year results September 24, 2010 Contents A strategy focused on healthcare Delivering strong results A strong financial structure Additional information 2 A strategy focused on healthcare 3

JSIam Introduction talk. Philippe Gradt. Grenoble, March 6th 2015

Introduction talk Philippe Gradt Grenoble, March 6th 2015 Introduction Invention Innovation Market validation is key. 1 Introduction Invention Innovation Market validation is key How to turn a product

Introduction talk Philippe Gradt Grenoble, March 6th 2015 Introduction Invention Innovation Market validation is key. 1 Introduction Invention Innovation Market validation is key How to turn a product

Don't put socks on the Hippopotamus. Bill BELT Emmanuel DE RYCKEL

Don't put socks on the Hippopotamus Bill BELT Emmanuel DE RYCKEL BEECHFIELD ASSOCIATES 2009 or you will screw up your Supply Chain. BEECHFIELD ASSOCIATES 2009 HIPPO ATTITUDE - inappropriate behavior -

Don't put socks on the Hippopotamus Bill BELT Emmanuel DE RYCKEL BEECHFIELD ASSOCIATES 2009 or you will screw up your Supply Chain. BEECHFIELD ASSOCIATES 2009 HIPPO ATTITUDE - inappropriate behavior -

CEPF FINAL PROJECT COMPLETION REPORT

CEPF FINAL PROJECT COMPLETION REPORT I. BASIC DATA Organization Legal Name: Conservation International Madagascar Project Title (as stated in the grant agreement): Knowledge Management: Information & Monitoring.

CEPF FINAL PROJECT COMPLETION REPORT I. BASIC DATA Organization Legal Name: Conservation International Madagascar Project Title (as stated in the grant agreement): Knowledge Management: Information & Monitoring.

Quatre axes au service de la performance et des mutations Four lines serve the performance and changes

Le Centre d Innovation des Technologies sans Contact-EuraRFID (CITC EuraRFID) est un acteur clé en matière de l Internet des Objets et de l Intelligence Ambiante. C est un centre de ressources, d expérimentations

Le Centre d Innovation des Technologies sans Contact-EuraRFID (CITC EuraRFID) est un acteur clé en matière de l Internet des Objets et de l Intelligence Ambiante. C est un centre de ressources, d expérimentations

Mise en place d un système de cabotage maritime au sud ouest de l Ocean Indien. 10 Septembre 2012

Mise en place d un système de cabotage maritime au sud ouest de l Ocean Indien 10 Septembre 2012 Les défis de la chaine de la logistique du transport maritime Danielle T.Y WONG Director Logistics Performance

Mise en place d un système de cabotage maritime au sud ouest de l Ocean Indien 10 Septembre 2012 Les défis de la chaine de la logistique du transport maritime Danielle T.Y WONG Director Logistics Performance

Forthcoming Database

DISS.ETH NO. 15802 Forthcoming Database A Framework Approach for Data Visualization Applications A dissertation submitted to the SWISS FEDERAL INSTITUTE OF TECHNOLOGY ZURICH for the degree of Doctor of

DISS.ETH NO. 15802 Forthcoming Database A Framework Approach for Data Visualization Applications A dissertation submitted to the SWISS FEDERAL INSTITUTE OF TECHNOLOGY ZURICH for the degree of Doctor of

La Poste choisit l'erp Open Source Compiere

La Poste choisit l'erp Open Source Compiere Redwood Shores, Calif. Compiere, Inc, leader mondial dans les progiciels de gestion Open Source annonce que La Poste, l'opérateur postal français, a choisi l'erp

La Poste choisit l'erp Open Source Compiere Redwood Shores, Calif. Compiere, Inc, leader mondial dans les progiciels de gestion Open Source annonce que La Poste, l'opérateur postal français, a choisi l'erp

PIB : Définition : mesure de l activité économique réalisée à l échelle d une nation sur une période donnée.

PIB : Définition : mesure de l activité économique réalisée à l échelle d une nation sur une période donnée. Il y a trois approches possibles du produit intérieur brut : Optique de la production Optique

PIB : Définition : mesure de l activité économique réalisée à l échelle d une nation sur une période donnée. Il y a trois approches possibles du produit intérieur brut : Optique de la production Optique

Préconisations pour une gouvernance efficace de la Manche. Pathways for effective governance of the English Channel

Préconisations pour une gouvernance efficace de la Manche Pathways for effective governance of the English Channel Prochaines étapes vers une gouvernance efficace de la Manche Next steps for effective

Préconisations pour une gouvernance efficace de la Manche Pathways for effective governance of the English Channel Prochaines étapes vers une gouvernance efficace de la Manche Next steps for effective

Small Businesses support Senator Ringuette s bill to limit credit card acceptance fees

For Immediate Release October 10, 2014 Small Businesses support Senator Ringuette s bill to limit credit card acceptance fees The Senate Standing Committee on Banking, Trade, and Commerce resumed hearings

For Immediate Release October 10, 2014 Small Businesses support Senator Ringuette s bill to limit credit card acceptance fees The Senate Standing Committee on Banking, Trade, and Commerce resumed hearings

Improving the breakdown of the Central Credit Register data by category of enterprises

Improving the breakdown of the Central Credit Register data by category of enterprises Workshop on Integrated management of micro-databases Deepening business intelligence within central banks statistical

Improving the breakdown of the Central Credit Register data by category of enterprises Workshop on Integrated management of micro-databases Deepening business intelligence within central banks statistical

Lean approach on production lines Oct 9, 2014

Oct 9, 2014 Dassault Mérignac 1 Emmanuel Théret Since sept. 2013 : Falcon 5X FAL production engineer 2011-2013 : chief project of 1st lean integration in Merignac plant 2010 : Falcon 7X FAL production

Oct 9, 2014 Dassault Mérignac 1 Emmanuel Théret Since sept. 2013 : Falcon 5X FAL production engineer 2011-2013 : chief project of 1st lean integration in Merignac plant 2010 : Falcon 7X FAL production

Le MDM (Master Data Management) Pierre angulaire d'une bonne stratégie de management de l'information

Pierre angulaire d'une bonne stratégie de management de l'information") Darren Cooper Information Management Consultant, IBM Software Group 1st December, 2011 Le MDM (Master Data Management) Pierre angulaire d'une bonne stratégie de management de l'information Information

Darren Cooper Information Management Consultant, IBM Software Group 1st December, 2011 Le MDM (Master Data Management) Pierre angulaire d'une bonne stratégie de management de l'information Information

that the child(ren) was/were in need of protection under Part III of the Child and Family Services Act, and the court made an order on

was/were in need of protection under Part III of the Child and Family Services Act, and the court made an order on") ONTARIO Court File Number at (Name of court) Court office address Applicant(s) (In most cases, the applicant will be a children s aid society.) Full legal name & address for service street & number, municipality,

ONTARIO Court File Number at (Name of court) Court office address Applicant(s) (In most cases, the applicant will be a children s aid society.) Full legal name & address for service street & number, municipality,

"Les outils de planification adaptés à la maîtrise d'un environnement incertain»

Association Française de Management FAPICS des Opérations de la Chaîne Logistique "Les outils de planification adaptés à la maîtrise d'un environnement incertain» La gestion de la performance commence

Association Française de Management FAPICS des Opérations de la Chaîne Logistique "Les outils de planification adaptés à la maîtrise d'un environnement incertain» La gestion de la performance commence

How to Login to Career Page

How to Login to Career Page BASF Canada July 2013 To view this instruction manual in French, please scroll down to page 16 1 Job Postings How to Login/Create your Profile/Sign Up for Job Posting Notifications

How to Login to Career Page BASF Canada July 2013 To view this instruction manual in French, please scroll down to page 16 1 Job Postings How to Login/Create your Profile/Sign Up for Job Posting Notifications

Discours du Ministre Tassarajen Pillay Chedumbrum. Ministre des Technologies de l'information et de la Communication (TIC) Worshop on Dot.

Worshop on Dot.") Discours du Ministre Tassarajen Pillay Chedumbrum Ministre des Technologies de l'information et de la Communication (TIC) Worshop on Dot.Mu Date: Jeudi 12 Avril 2012 L heure: 9h15 Venue: Conference Room,

Discours du Ministre Tassarajen Pillay Chedumbrum Ministre des Technologies de l'information et de la Communication (TIC) Worshop on Dot.Mu Date: Jeudi 12 Avril 2012 L heure: 9h15 Venue: Conference Room,

Scénarios économiques en assurance

Motivation et plan du cours Galea & Associés ISFA - Université Lyon 1 ptherond@galea-associes.eu pierre@therond.fr 18 octobre 2013 Motivation Les nouveaux référentiels prudentiel et d'information nancière

Motivation et plan du cours Galea & Associés ISFA - Université Lyon 1 ptherond@galea-associes.eu pierre@therond.fr 18 octobre 2013 Motivation Les nouveaux référentiels prudentiel et d'information nancière

AUDIT COMMITTEE: TERMS OF REFERENCE

AUDIT COMMITTEE: TERMS OF REFERENCE PURPOSE The Audit Committee (the Committee), assists the Board of Trustees to fulfill its oversight responsibilities to the Crown, as shareholder, for the following

AUDIT COMMITTEE: TERMS OF REFERENCE PURPOSE The Audit Committee (the Committee), assists the Board of Trustees to fulfill its oversight responsibilities to the Crown, as shareholder, for the following

BNP Paribas Personal Finance

BNP Paribas Personal Finance Financially fragile loan holder prevention program CUSTOMERS IN DIFFICULTY: QUICKER IDENTIFICATION MEANS BETTER SUPPORT Brussels, December 12th 2014 Why BNPP PF has developed

BNP Paribas Personal Finance Financially fragile loan holder prevention program CUSTOMERS IN DIFFICULTY: QUICKER IDENTIFICATION MEANS BETTER SUPPORT Brussels, December 12th 2014 Why BNPP PF has developed

Optimiser votre reporting sans déployer BW

Optimiser votre reporting sans déployer BW Exploiter nos données opérationnelles Peut-on faire du reporting directement sur ECC sans datawarehouse? Agenda La suite BusinessObjects intégrée à ECC 3 scénarios

Optimiser votre reporting sans déployer BW Exploiter nos données opérationnelles Peut-on faire du reporting directement sur ECC sans datawarehouse? Agenda La suite BusinessObjects intégrée à ECC 3 scénarios

Performance Management Systems

Master en ingénieur de gestion Performance Management Systems Finalité spécialisée du Master en ingénieur de gestion Introduction La finalité spécialisée Performance Management Systems intéressera en

Master en ingénieur de gestion Performance Management Systems Finalité spécialisée du Master en ingénieur de gestion Introduction La finalité spécialisée Performance Management Systems intéressera en

Frequently Asked Questions

GS1 Canada-1WorldSync Partnership Frequently Asked Questions 1. What is the nature of the GS1 Canada-1WorldSync partnership? GS1 Canada has entered into a partnership agreement with 1WorldSync for the

GS1 Canada-1WorldSync Partnership Frequently Asked Questions 1. What is the nature of the GS1 Canada-1WorldSync partnership? GS1 Canada has entered into a partnership agreement with 1WorldSync for the

Formulaire d inscription (form also available in English) Mission commerciale en Floride. Coordonnées

Mission commerciale en Floride. Coordonnées") Formulaire d inscription (form also available in English) Mission commerciale en Floride Mission commerciale Du 29 septembre au 2 octobre 2015 Veuillez remplir un formulaire par participant Coordonnées

Formulaire d inscription (form also available in English) Mission commerciale en Floride Mission commerciale Du 29 septembre au 2 octobre 2015 Veuillez remplir un formulaire par participant Coordonnées

Plan de la présentation

Etude comparative des pratiques de l intelligence économique entre le Maroc, l Afrique du Sud et le Brésil Par: Mourad Oubrich 3 Plan de la présentation Contexte Cadre conceptuel de l IE Etude empirique

Etude comparative des pratiques de l intelligence économique entre le Maroc, l Afrique du Sud et le Brésil Par: Mourad Oubrich 3 Plan de la présentation Contexte Cadre conceptuel de l IE Etude empirique

The impacts of m-payment on financial services Novembre 2011

The impacts of m-payment on financial services Novembre 2011 3rd largest European postal operator by turnover The most diversified European postal operator with 3 business lines 2010 Turnover Mail 52%

The impacts of m-payment on financial services Novembre 2011 3rd largest European postal operator by turnover The most diversified European postal operator with 3 business lines 2010 Turnover Mail 52%

THÈSE. présentée à TÉLÉCOM PARISTECH. pour obtenir le grade de. DOCTEUR de TÉLÉCOM PARISTECH. Mention Informatique et Réseaux. par.

École Doctorale d Informatique, Télécommunications et Électronique de Paris THÈSE présentée à TÉLÉCOM PARISTECH pour obtenir le grade de DOCTEUR de TÉLÉCOM PARISTECH Mention Informatique et Réseaux par

École Doctorale d Informatique, Télécommunications et Électronique de Paris THÈSE présentée à TÉLÉCOM PARISTECH pour obtenir le grade de DOCTEUR de TÉLÉCOM PARISTECH Mention Informatique et Réseaux par

L impact des délais de paiement et des solutions appropriées. Dominique Geenens Intrum Justitia

L impact des délais de paiement et des solutions appropriées Dominique Geenens Intrum Justitia Groupe Intrum Justitia Leader du marché en gestion de crédit Entreprise européenne dynamique avec siège principal

L impact des délais de paiement et des solutions appropriées Dominique Geenens Intrum Justitia Groupe Intrum Justitia Leader du marché en gestion de crédit Entreprise européenne dynamique avec siège principal

Exemple PLS avec SAS

Exemple PLS avec SAS This example, from Umetrics (1995), demonstrates different ways to examine a PLS model. The data come from the field of drug discovery. New drugs are developed from chemicals that

Exemple PLS avec SAS This example, from Umetrics (1995), demonstrates different ways to examine a PLS model. The data come from the field of drug discovery. New drugs are developed from chemicals that

RAPID 3.34 - Prenez le contrôle sur vos données

RAPID 3.34 - Prenez le contrôle sur vos données Parmi les fonctions les plus demandées par nos utilisateurs, la navigation au clavier et la possibilité de disposer de champs supplémentaires arrivent aux

RAPID 3.34 - Prenez le contrôle sur vos données Parmi les fonctions les plus demandées par nos utilisateurs, la navigation au clavier et la possibilité de disposer de champs supplémentaires arrivent aux

Gestion des prestations Volontaire

Gestion des prestations Volontaire Qu estce que l Income Management (Gestion des prestations)? La gestion des prestations est un moyen de vous aider à gérer votre argent pour couvrir vos nécessités et

Gestion des prestations Volontaire Qu estce que l Income Management (Gestion des prestations)? La gestion des prestations est un moyen de vous aider à gérer votre argent pour couvrir vos nécessités et

Projet de réorganisation des activités de T-Systems France

Informations aux medias Saint-Denis, France, 13 Février 2013 Projet de réorganisation des activités de T-Systems France T-Systems France a présenté à ses instances représentatives du personnel un projet

Informations aux medias Saint-Denis, France, 13 Février 2013 Projet de réorganisation des activités de T-Systems France T-Systems France a présenté à ses instances représentatives du personnel un projet

Sustainability Monitoring and Reporting: Tracking Your Community s Sustainability Performance

Sustainability Monitoring and Reporting: Tracking Your Community s Sustainability Performance Thursday, February 11 th, 2011 FCM Sustainable Communities Conference, Victoria, BC The Agenda 1. Welcome and

Sustainability Monitoring and Reporting: Tracking Your Community s Sustainability Performance Thursday, February 11 th, 2011 FCM Sustainable Communities Conference, Victoria, BC The Agenda 1. Welcome and

La solution idéale de personnalisation interactive sur internet

FACTORY121 Product Configurator (summary) La solution idéale de personnalisation interactive sur internet FACTORY121 cité comme référence en «Mass Customization» au MIT et sur «mass-customization.de» Specifications

FACTORY121 Product Configurator (summary) La solution idéale de personnalisation interactive sur internet FACTORY121 cité comme référence en «Mass Customization» au MIT et sur «mass-customization.de» Specifications

Compléter le formulaire «Demande de participation» et l envoyer aux bureaux de SGC* à l adresse suivante :

FOIRE AUX QUESTIONS COMMENT ADHÉRER? Compléter le formulaire «Demande de participation» et l envoyer aux bureaux de SGC* à l adresse suivante : 275, boul des Braves Bureau 310 Terrebonne (Qc) J6W 3H6 La

FOIRE AUX QUESTIONS COMMENT ADHÉRER? Compléter le formulaire «Demande de participation» et l envoyer aux bureaux de SGC* à l adresse suivante : 275, boul des Braves Bureau 310 Terrebonne (Qc) J6W 3H6 La

RULE 5 - SERVICE OF DOCUMENTS RÈGLE 5 SIGNIFICATION DE DOCUMENTS. Rule 5 / Règle 5

RULE 5 - SERVICE OF DOCUMENTS General Rules for Manner of Service Notices of Application and Other Documents 5.01 (1) A notice of application or other document may be served personally, or by an alternative

RULE 5 - SERVICE OF DOCUMENTS General Rules for Manner of Service Notices of Application and Other Documents 5.01 (1) A notice of application or other document may be served personally, or by an alternative

PRESENTATION. CRM Paris - 19/21 rue Hélène Boucher - ZA Chartres Est - Jardins d'entreprises - 28 630 GELLAINVILLE

PRESENTATION Spécialités Chimiques Distribution entreprise créée en 1997, a répondu à cette époque à la demande du grand chimiquier HOECHTS (CLARIANT) pour distribuer différents ingrédients en petites

PRESENTATION Spécialités Chimiques Distribution entreprise créée en 1997, a répondu à cette époque à la demande du grand chimiquier HOECHTS (CLARIANT) pour distribuer différents ingrédients en petites

Consultants en coûts - Cost Consultants

Respecter l échéancier et le budget est-ce possible? On time, on budget is it possible? May, 2010 Consultants en coûts - Cost Consultants Boulletin/Newsletter Volume 8 Mai ( May),2010 1 866 694 6494 info@emangepro.com

Respecter l échéancier et le budget est-ce possible? On time, on budget is it possible? May, 2010 Consultants en coûts - Cost Consultants Boulletin/Newsletter Volume 8 Mai ( May),2010 1 866 694 6494 info@emangepro.com

The new consumables catalogue from Medisoft is now updated. Please discover this full overview of all our consumables available to you.

General information 120426_CCD_EN_FR Dear Partner, The new consumables catalogue from Medisoft is now updated. Please discover this full overview of all our consumables available to you. To assist navigation

General information 120426_CCD_EN_FR Dear Partner, The new consumables catalogue from Medisoft is now updated. Please discover this full overview of all our consumables available to you. To assist navigation

PAR RINOX INC BY RINOX INC PROGRAMME D INSTALLATEUR INSTALLER PROGRAM

PAR RINOX INC BY RINOX INC PROGRAMME D INSTALLATEUR INSTALLER PROGRAM DEVENEZ UN RINOXPERT DÈS AUJOURD HUI! BECOME A RINOXPERT NOW OPTIMISER VOS VENTES INCREASE YOUR SALES VISIBILITÉ & AVANTAGES VISIBILITY

PAR RINOX INC BY RINOX INC PROGRAMME D INSTALLATEUR INSTALLER PROGRAM DEVENEZ UN RINOXPERT DÈS AUJOURD HUI! BECOME A RINOXPERT NOW OPTIMISER VOS VENTES INCREASE YOUR SALES VISIBILITÉ & AVANTAGES VISIBILITY

UML : Unified Modeling Language

UML : Unified Modeling Language Recommended: UML distilled A brief guide to the standard Object Modeling Language Addison Wesley based on Frank Maurer lecture, Univ. of Calgary in french : uml.free.fr/index.html

UML : Unified Modeling Language Recommended: UML distilled A brief guide to the standard Object Modeling Language Addison Wesley based on Frank Maurer lecture, Univ. of Calgary in french : uml.free.fr/index.html

COUNCIL OF THE EUROPEAN UNION. Brussels, 18 September 2008 (19.09) (OR. fr) 13156/08 LIMITE PI 53

(OR. fr) 13156/08 LIMITE PI 53") COUNCIL OF THE EUROPEAN UNION Brussels, 18 September 2008 (19.09) (OR. fr) 13156/08 LIMITE PI 53 WORKING DOCUMENT from : Presidency to : delegations No prev. doc.: 12621/08 PI 44 Subject : Revised draft

COUNCIL OF THE EUROPEAN UNION Brussels, 18 September 2008 (19.09) (OR. fr) 13156/08 LIMITE PI 53 WORKING DOCUMENT from : Presidency to : delegations No prev. doc.: 12621/08 PI 44 Subject : Revised draft

Institut français des sciences et technologies des transports, de l aménagement

Institut français des sciences et technologies des transports, de l aménagement et des réseaux Session 3 Big Data and IT in Transport: Applications, Implications, Limitations Jacques Ehrlich/IFSTTAR h/ifsttar

Institut français des sciences et technologies des transports, de l aménagement et des réseaux Session 3 Big Data and IT in Transport: Applications, Implications, Limitations Jacques Ehrlich/IFSTTAR h/ifsttar

INVESTMENT REGULATIONS R-090-2001 In force October 1, 2001. RÈGLEMENT SUR LES INVESTISSEMENTS R-090-2001 En vigueur le 1 er octobre 2001

FINANCIAL ADMINISTRATION ACT INVESTMENT REGULATIONS R-090-2001 In force October 1, 2001 LOI SUR LA GESTION DES FINANCES PUBLIQUES RÈGLEMENT SUR LES INVESTISSEMENTS R-090-2001 En vigueur le 1 er octobre

FINANCIAL ADMINISTRATION ACT INVESTMENT REGULATIONS R-090-2001 In force October 1, 2001 LOI SUR LA GESTION DES FINANCES PUBLIQUES RÈGLEMENT SUR LES INVESTISSEMENTS R-090-2001 En vigueur le 1 er octobre

ADHEFILM : tronçonnage. ADHEFILM : cutting off. ADHECAL : fabrication. ADHECAL : manufacturing.

LA MAÎTRISE D UN MÉTIER Depuis plus de 20 ans, ADHETEC construit sa réputation sur la qualité de ses films adhésifs. Par la maîtrise de notre métier, nous apportons à vos applications la force d une offre

LA MAÎTRISE D UN MÉTIER Depuis plus de 20 ans, ADHETEC construit sa réputation sur la qualité de ses films adhésifs. Par la maîtrise de notre métier, nous apportons à vos applications la force d une offre

Discours de Eric Lemieux Sommet Aéro Financement Palais des congrès, 4 décembre 2013

Discours de Eric Lemieux Sommet Aéro Financement Palais des congrès, 4 décembre 2013 Bonjour Mesdames et Messieurs, Je suis très heureux d être avec vous aujourd hui pour ce Sommet AéroFinancement organisé

Discours de Eric Lemieux Sommet Aéro Financement Palais des congrès, 4 décembre 2013 Bonjour Mesdames et Messieurs, Je suis très heureux d être avec vous aujourd hui pour ce Sommet AéroFinancement organisé

Regulation and governance through performance in the service management contract

Regulation and governance through performance in the service management contract Agathe Cohen- Syndicat des eaux d'ile-de-france Florence- séminaire du 7 et 8 février 2013 Summary 1- Key figures of SEDIF

Regulation and governance through performance in the service management contract Agathe Cohen- Syndicat des eaux d'ile-de-france Florence- séminaire du 7 et 8 février 2013 Summary 1- Key figures of SEDIF

Un système KYC robuste et sa valeur ajoutée commerciale

MY JOURNEY BEGAN AT 19, WHEN I LANDED IN THE COLDEST PLACE I D EVER EXPERIENCED. MAJID AL-NASSAR BUSINESS OWNER AND PROPERTY INVESTOR. EVERY JOURNEY IS UNIQUE. Un système KYC robuste et sa valeur ajoutée

MY JOURNEY BEGAN AT 19, WHEN I LANDED IN THE COLDEST PLACE I D EVER EXPERIENCED. MAJID AL-NASSAR BUSINESS OWNER AND PROPERTY INVESTOR. EVERY JOURNEY IS UNIQUE. Un système KYC robuste et sa valeur ajoutée

Support Orders and Support Provisions (Banks and Authorized Foreign Banks) Regulations

Regulations") CANADA CONSOLIDATION CODIFICATION Support Orders and Support Provisions (Banks and Authorized Foreign Banks) Regulations Règlement sur les ordonnances alimentaires et les dispositions alimentaires (banques

CANADA CONSOLIDATION CODIFICATION Support Orders and Support Provisions (Banks and Authorized Foreign Banks) Regulations Règlement sur les ordonnances alimentaires et les dispositions alimentaires (banques

SAP SNC (Supply Network Collaboration) Web Package. (Français / English) language. Edition 2013 Mars

Web Package. (Français / English) language. Edition 2013 Mars") SAP SNC (Supply Network Collaboration) Web Package (Français / English) language Edition 2013 Mars Direction des Achats Philippe.longuet@sagemcom.com Date: 28/03/13 Sagemcom portal Content of presentation

SAP SNC (Supply Network Collaboration) Web Package (Français / English) language Edition 2013 Mars Direction des Achats Philippe.longuet@sagemcom.com Date: 28/03/13 Sagemcom portal Content of presentation

22 ème congrès Fapics

22 ème congrès Fapics Invités par et avec la contribution de : Grâce à nos partenaires : Instituts de formation 22 ème congrès Fapics Cabinets de conseil : Grâce à nos sponsors : 22 ème congrès Fapics

22 ème congrès Fapics Invités par et avec la contribution de : Grâce à nos partenaires : Instituts de formation 22 ème congrès Fapics Cabinets de conseil : Grâce à nos sponsors : 22 ème congrès Fapics

La gestion des risques IT et l audit

La gestion des risques IT et l audit 5èmé rencontre des experts auditeurs en sécurité de l information De l audit au management de la sécurité des systèmes d information 14 Février 2013 Qui sommes nous?

La gestion des risques IT et l audit 5èmé rencontre des experts auditeurs en sécurité de l information De l audit au management de la sécurité des systèmes d information 14 Février 2013 Qui sommes nous?

Toni Lazazzera toni.lazazzera@tmanco.com. Tmanco is expert partner from Anatole (www.anatole.net) and distributes the solution AnatoleTEM

and distributes the solution AnatoleTEM") T e l e c o m m a n a g e m e n t c o m p e t e n c e Toni Lazazzera toni.lazazzera@tmanco.com Tmanco SA CH 6807 Taverne www.tmanco.com +41 91 930 96 63 Reduce your telecom invoices up to 30% through better

T e l e c o m m a n a g e m e n t c o m p e t e n c e Toni Lazazzera toni.lazazzera@tmanco.com Tmanco SA CH 6807 Taverne www.tmanco.com +41 91 930 96 63 Reduce your telecom invoices up to 30% through better

THE WEX FLEET CARD A NEW WAY FOR BUSINESSES TO FUEL VEHICLES

THE WEX FLEET CARD A NEW WAY FOR BUSINESSES TO FUEL VEHICLES Many business managers use debit cards, credit cards, or even cash to fuel their vehicles. This leads to the administrative hassles of sorting

THE WEX FLEET CARD A NEW WAY FOR BUSINESSES TO FUEL VEHICLES Many business managers use debit cards, credit cards, or even cash to fuel their vehicles. This leads to the administrative hassles of sorting

The WEX FLEET Card. A new way for businesses to fuel vehicles

TM The WEX FLEET Card A new way for businesses to fuel vehicles Many business managers use debit cards, credit cards, or even cash to fuel their vehicles. This leads to the administrative hassles of sorting

TM The WEX FLEET Card A new way for businesses to fuel vehicles Many business managers use debit cards, credit cards, or even cash to fuel their vehicles. This leads to the administrative hassles of sorting

AXES MANAGEMENT CONSULTING. Le partage des valeurs, la recherche de la performance. Sharing values, improving performance

AXES MANAGEMENT CONSULTING Le partage des valeurs, la recherche de la performance Sharing values, improving performance Abeille (apis) : les abeilles facilitent la pollinisation en passant d une fleur

AXES MANAGEMENT CONSULTING Le partage des valeurs, la recherche de la performance Sharing values, improving performance Abeille (apis) : les abeilles facilitent la pollinisation en passant d une fleur

Eléments de statistique

Eléments de statistique L. Wehenkel Cours du 9/12/2014 Méthodes multivariées; applications & recherche Quelques méthodes d analyse multivariée NB: illustration sur base de la BD résultats de probas en

Eléments de statistique L. Wehenkel Cours du 9/12/2014 Méthodes multivariées; applications & recherche Quelques méthodes d analyse multivariée NB: illustration sur base de la BD résultats de probas en

Paxton. ins-20605. Net2 desktop reader USB

Paxton ins-20605 Net2 desktop reader USB 1 3 2 4 1 2 Desktop Reader The desktop reader is designed to sit next to the PC. It is used for adding tokens to a Net2 system and also for identifying lost cards.

Paxton ins-20605 Net2 desktop reader USB 1 3 2 4 1 2 Desktop Reader The desktop reader is designed to sit next to the PC. It is used for adding tokens to a Net2 system and also for identifying lost cards.

CRM Company Group lance l offre volontaire de rachat en espèces des 2 100 OC 1 restant en circulation.

CORPORATE EVENT NOTICE: Offre volontaire de rachat CRM COMPANY GROUP PLACE: Paris AVIS N : PAR_20121121_10423_ALT DATE: 21/11/2012 MARCHE: Alternext Paris CRM Company Group lance l offre volontaire de

CORPORATE EVENT NOTICE: Offre volontaire de rachat CRM COMPANY GROUP PLACE: Paris AVIS N : PAR_20121121_10423_ALT DATE: 21/11/2012 MARCHE: Alternext Paris CRM Company Group lance l offre volontaire de

Deadline(s): Assignment: in week 8 of block C Exam: in week 7 (oral exam) and in the exam week (written exam) of block D

: Assignment: in week 8 of block C Exam: in week 7 (oral exam) and in the exam week (written exam) of block D") ICM STUDENT MANUAL French 2 JIC-FRE2.2V-12 Module Change Management and Media Research Study Year 2 1. Course overview Books: Français.com, niveau intermédiaire, livre d élève+ dvd- rom, 2ième édition,

ICM STUDENT MANUAL French 2 JIC-FRE2.2V-12 Module Change Management and Media Research Study Year 2 1. Course overview Books: Français.com, niveau intermédiaire, livre d élève+ dvd- rom, 2ième édition,

Editing and managing Systems engineering processes at Snecma

Editing and managing Systems engineering processes at Snecma Atego workshop 2014-04-03 Ce document et les informations qu il contient sont la propriété de Ils ne doivent pas être copiés ni communiqués

Editing and managing Systems engineering processes at Snecma Atego workshop 2014-04-03 Ce document et les informations qu il contient sont la propriété de Ils ne doivent pas être copiés ni communiqués

Contrôle d'accès Access control. Notice technique / Technical Manual